fredpy Examples¶

[1]:

import pandas as pd

import numpy as np

import fredpy as fp

import matplotlib.pyplot as plt

# Use matplotlib's 'classic' style, set figure facecolor to white

plt.style.use('classic')

plt.rcParams.update({'figure.facecolor': 'white'})

Load API key¶

First apply for an API key for FRED here: https://research.stlouisfed.org/docs/api/api_key.html. The API key is a 32 character string that is required for making requests from FRED. Save your API key in the fp namespace by either setting the fp.api_key directly:

[2]:

fp.api_key = '################################'

or by reading from a text file containing only the text of the API key in the first line:

[3]:

fp.api_key = fp.load_api_key('fred_api_key.txt')

If fred_api_key.txt is not in the same directory as your program file, then you must supply the full path of the file.

Preliminary example¶

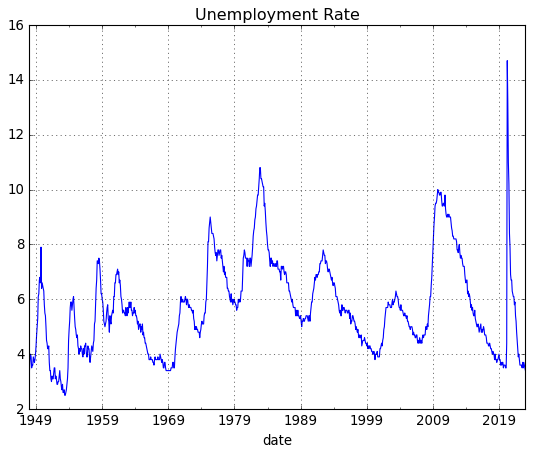

Downloading and plotting unemployment rate data for the US is easy with fredpy:

[4]:

fig = plt.figure()

u = fp.series('UNRATE')

plt.plot(u.data.index,u.data.values,'-',lw=3,alpha = 0.65)

plt.grid()

plt.ylabel('Percent');

A closer look at fredpy using real GDP data¶

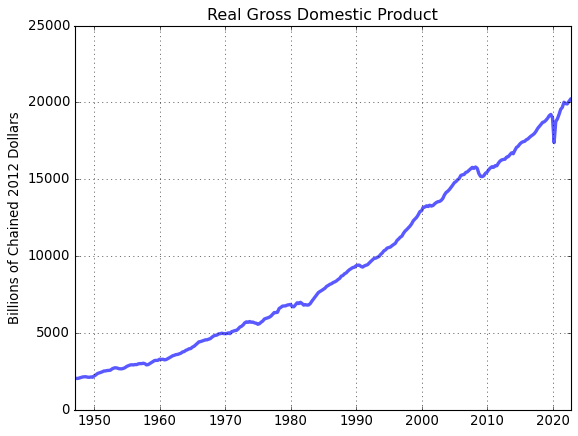

Use fredpy to download real GDP data. The FRED page for real GDP: https://fred.stlouisfed.org/series/GDPC1. Note that the series ID - GDPC1 - is in the URL and is visible in several places on the page.

The data in text format is located at: https://fred.stlouisfed.org/data/gdpc1.txt. When supplied with the series ID GDPC1, fredpy visits the the URL for the text-formatted data, reads the information on the page, and stores the data as attributes of a fredpy.series instance.

[5]:

# Download quarterly real GDP data using `fredpy`. Save the data in a variable called gdp

gdp = fp.series('gdpc1')

# Note that gdp is an instance of the `fredpy.series` class

print(type(gdp))

<class 'fredpy.series'>

Attributes¶

A fredpy.series instance stores information about a FRED series in 17 attribues:

data: (Pandas Series) - data values.

date_range: (string) - specifies the dates of the first and last observations.

frequency: (string) - data frequency. ‘Daily’, ‘Weekly’, ‘Monthly’, ‘Quarterly’, ‘Semiannual’, or ‘Annual’.

frequency_short: (string) - data frequency. Abbreviated. ‘D’, ‘W’, ‘M’, ‘Q’, ‘SA, or ‘A’.

last_updated: (string) - date series was last updated.

notes: (string) - details about series. Not available for all series.

observation_date: (string) – vintage date at which data are observed.

release: (string) - statistical release containing data.

seasonal_adjustment: (string) - specifies whether the data has been seasonally adjusted.

seasonal_adjustment_short: (string) - specifies whether the data has been seasonally adjusted. Abbreviated.

series_id: (string) - unique FRED series ID code.

source: (string) - original source of the data.

t: (int) - number corresponding to frequency: 365 for daily, 52 for weekly, 12 for monthly, 4 for quarterly, and 1 for annual.

title: (string) - title of the data series.

units: (string) - units of the data series.

units_short: (string) - units of the data series. Abbreviated.

[6]:

# Print the title, the units, the frequency, the date range, and the source of the gdp data

print(gdp.title)

print(gdp.units)

print(gdp.frequency)

print(gdp.date_range)

print(gdp.source)

Real Gross Domestic Product

Billions of Chained 2012 Dollars

Quarterly

Range: 1947-01-01 to 2022-10-01

U.S. Bureau of Economic Analysis

[7]:

# Print the last 4 values of the gdp data

print(gdp.data[-4:],'\n')

date

2022-01-01 19924.088

2022-04-01 19895.271

2022-07-01 20054.663

2022-10-01 20198.091

Freq: QS-OCT, Name: value, dtype: float64

[8]:

# Plot real GDP data

fig = plt.figure()

ax = fig.add_subplot(1,1,1)

ax.plot(gdp.data,'-',lw=3,alpha = 0.65)

ax.grid()

ax.set_title(gdp.title)

ax.set_ylabel(gdp.units);

Methods¶

A fredpy.series instance has 20 methods:

apc(log=False, backward=True)

as_frequency(freq=None,method=’mean’)

bp_filter(low=6, high=32, K=12)

cf_filter(low=6, high=32)

copy()

diff_filter()

divide(object2)

dropn_nan()

hp_filter(lamb=1600)

linear_filter()

log()

ma(length,center=False)

minus(object2)

pc(log=False, backward=True, annualized=False)

per_capita(total_pop=True)

plot(**kwargs)

plus(object2)

recent(N)

recessions(color=’0.5’, alpha = 0.5)

times(object2)

window(win)

The fredpy documentation has detailed explanations of the use of these methods: https://www.briancjenkins.com/fredpy/docs/build/html/series_class.html.

[9]:

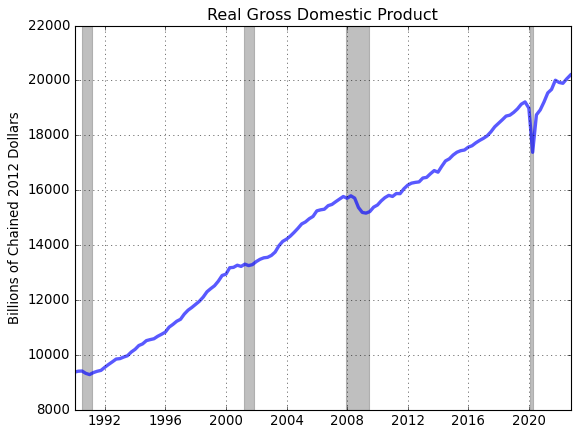

# Restrict GDP to observations from January 1, 1990 to present

win = ['01-01-1990','01-01-2200']

gdp_win = gdp.window(win)

# Plot

fig = plt.figure()

ax = fig.add_subplot(1,1,1)

ax.plot(gdp_win.data,'-',lw=3,alpha = 0.65)

ax.grid()

ax.set_title(gdp_win.title)

ax.set_ylabel(gdp_win.units)

# Plot recession bars

gdp_win.recessions()

[10]:

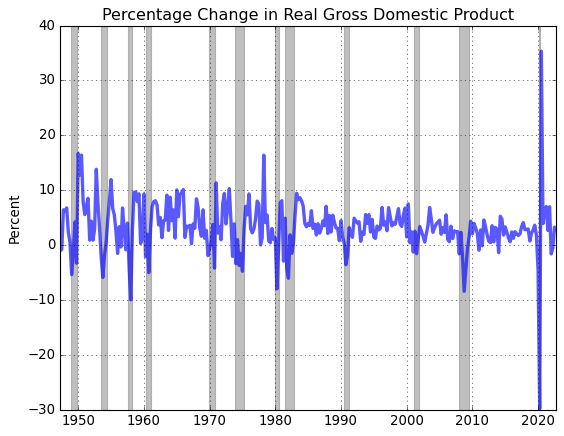

# Compute and plot the (annualized) quarterly growth rate of real GDP

gdp_pc = gdp.pc(annualized=True)

# Plot

fig = plt.figure()

ax = fig.add_subplot(1,1,1)

ax.plot(gdp_pc.data,'-',lw=3,alpha = 0.65)

ax.grid()

ax.set_title(gdp_pc.title)

ax.set_ylabel(gdp_pc.units)

# Plot recession bars

gdp_pc.recessions()

[11]:

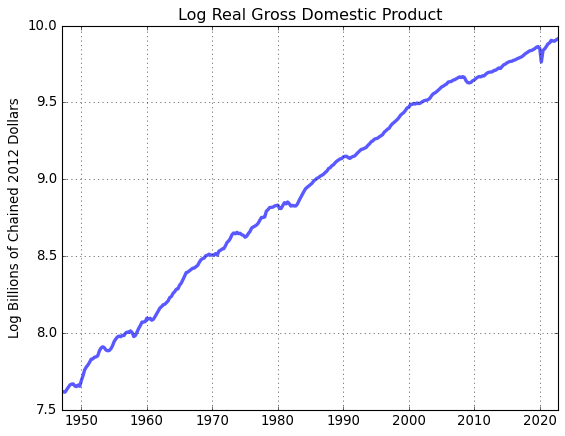

# Compute and plot the log of real GDP

gdp_log = gdp.log()

# Plot

fig = plt.figure()

ax = fig.add_subplot(1,1,1)

ax.plot(gdp_log.data,'-',lw=3,alpha = 0.65)

ax.set_title(gdp_log.title)

ax.set_ylabel(gdp_log.units)

ax.grid()

More examples¶

The following examples demonstrate some additional fredpy functionality.

Comparison of CPI and GDP deflator inflation¶

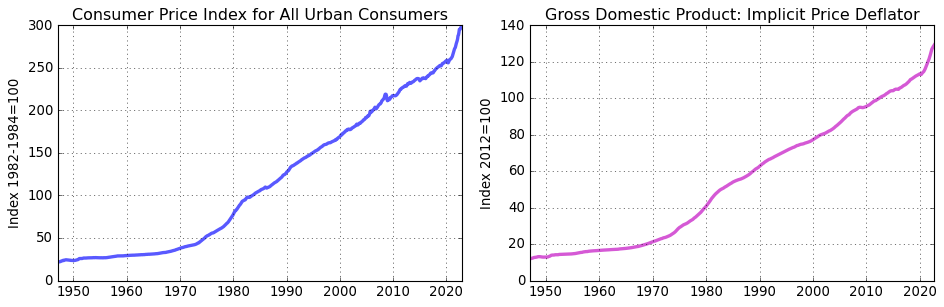

CPI data are released monthly by the BLS while GDP deflator data are released quarterly by the BEA. Here we’ll first convert the monthly CPI data to monthly frequency compute inflation as the percentage change in the respective index since on year prior.

[12]:

# Download CPI and GDP deflator data

cpi = fp.series('CPIAUCSL')

deflator = fp.series('GDPDEF')

fig = plt.figure(figsize=(12,4))

ax = fig.add_subplot(1,2,1)

ax.plot(cpi.data,'-',lw=3,alpha = 0.65)

ax.grid()

ax.set_title(cpi.title.split(':')[0])

ax.set_ylabel(cpi.units)

ax = fig.add_subplot(1,2,2)

ax.plot(deflator.data,'-m',lw=3,alpha = 0.65)

ax.grid()

ax.set_title(deflator.title)

ax.set_ylabel(deflator.units)

# Imporove use of whitespace

fig.tight_layout()

[13]:

# The CPI data are produced at a monthly frequency

print(cpi.frequency)

# Convert CPI data to quarterly frequency to conform with the GDP deflator

cpi_Q = cpi.as_frequency(freq='Q')

print(cpi_Q.frequency)

Monthly

Quarterly

[14]:

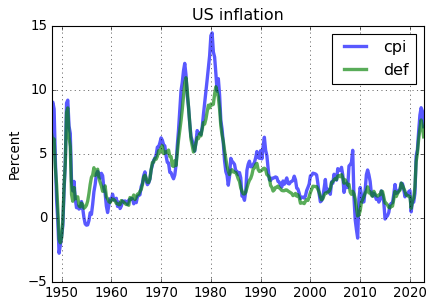

# Compute the inflation rate based on each index

cpi_pi = cpi_Q.apc()

def_pi = deflator.apc()

# Print date ranges for new inflation series

print(cpi_pi.date_range)

print(def_pi.date_range)

Range: 1948-01-01 to 2022-10-01

Range: 1948-01-01 to 2022-10-01

[15]:

fig = plt.figure(figsize=(6,4))

ax = fig.add_subplot(1,1,1)

ax.plot(cpi_pi.data,'-',lw=3,alpha = 0.65,label='cpi')

ax.plot(def_pi.data,'-',lw=3,alpha = 0.65,label='def')

ax.legend(loc='upper right')

ax.set_title('US inflation')

ax.set_ylabel('Percent')

ax.grid()

Even though the CPI inflation rate is on average about .3% higher the GDP deflator inflation rate, the CPI and the GDP deflator produce comparable measures of US inflation.

Equalizing date ranges of different series¶

Often data series have different observation ranges. The fredpy.window_equalize() function provides a quick way to set the date ranges for multiple series to the same interval.

[16]:

# Download unemployment and 3 month T-bill data

unemp = fp.series('UNRATE')

tbill_3m = fp.series('TB3MS')

# Print date ranges for series

print(unemp.date_range)

print(tbill_3m.date_range)

# Equalize the date ranges

unemp, tbill_3m = fp.window_equalize([unemp, tbill_3m])

# Print the new date ranges for series

print()

print(unemp.date_range)

print(tbill_3m.date_range)

Range: 1948-01-01 to 2023-01-01

Range: 1934-01-01 to 2023-01-01

Range: 1948-01-01 to 2023-01-01

Range: 1948-01-01 to 2023-01-01

Filtering 1: Extracting business cycle components from quarterly data with the HP filter¶

[17]:

# Download nominal GDP, the GDP deflator

gdp = fp.series('GDP')

defl = fp.series('GDPDEF')

# Make sure that all series have the same window of observation

gdp,defl = fp.window_equalize([gdp,defl])

# Deflate GDP series

gdp = gdp.divide(defl)

# Convert GDP to per capita terms

gdp = gdp.per_capita()

# Take log of GDP

gdp = gdp.log()

[18]:

# Plot log data

fig = plt.figure(figsize=(6,4))

ax1 = fig.add_subplot(1,1,1)

ax1.plot(gdp.data,'-',lw=3,alpha = 0.65)

ax1.grid()

ax1.set_title('log real GDP per capita')

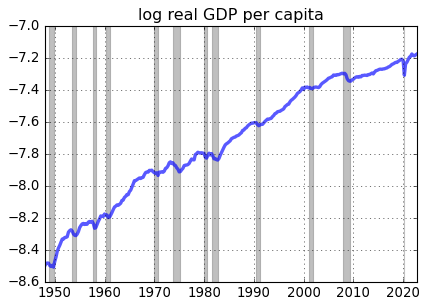

gdp.recessions()

The post-Great Recession slowdown in US real GDP growth is apparent in the figure.

[19]:

# Compute the hpfilter

gdp_cycle, gdp_trend = gdp.hp_filter()

[20]:

# Plot log data

fig = plt.figure(figsize=(6,8))

ax1 = fig.add_subplot(2,1,1)

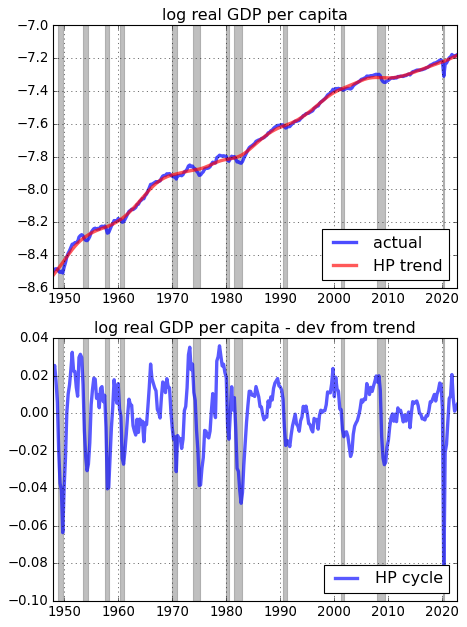

ax1.plot(gdp.data,'-',lw=3,alpha = 0.7,label='actual')

ax1.plot(gdp_trend.data,'r-',lw=3,alpha = 0.65,label='HP trend')

ax1.grid()

ax1.set_title('log real GDP per capita')

gdp.recessions()

ax1.legend(loc='lower right')

fig.tight_layout()

ax1 = fig.add_subplot(2,1,2)

ax1.plot(gdp_cycle.data,'b-',lw=3,alpha = 0.65,label='HP cycle')

ax1.grid()

ax1.set_title('log real GDP per capita - dev from trend')

gdp.recessions()

ax1.legend(loc='lower right')

# Imporove use of whitespace

fig.tight_layout()

Filtering 2: Extracting business cycle components from monthly data¶

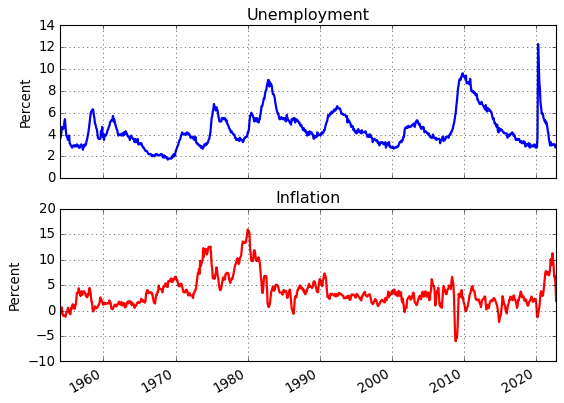

In Figure 1.5 from The Conquest of American Inflation, Thomas Sargent compares the business cycle componenets (BP filtered) of monthly inflation and unemployment data for the US from 1960-1982. Here we replicate Figure 1.5 to include the most recently available data and we also consturct the figure using HP filtered data.

[21]:

u = fp.series('LNS14000028')

p = fp.series('CPIAUCSL')

# Construct the inflation series

p = p.pc(annualized=True)

p = p.ma(length=6,center=True)

# Make sure that the data inflation and unemployment series cver the same time interval

p,u = fp.window_equalize([p,u])

# Data

fig = plt.figure()

ax = fig.add_subplot(2,1,1)

ax.plot(u.data,'b-',lw=2)

ax.grid(True)

ax.set_title('Unemployment')

ax.set_ylabel('Percent')

ax = fig.add_subplot(2,1,2)

ax.plot(p.data,'r-',lw=2)

ax.grid(True)

ax.set_title('Inflation')

ax.set_ylabel('Percent')

fig.autofmt_xdate()

[22]:

# Filter the data

p_bpcycle,p_bptrend = p.bp_filter(low=24,high=84,K=84)

u_bpcycle,u_bptrend = u.bp_filter(low=24,high=84,K=84)

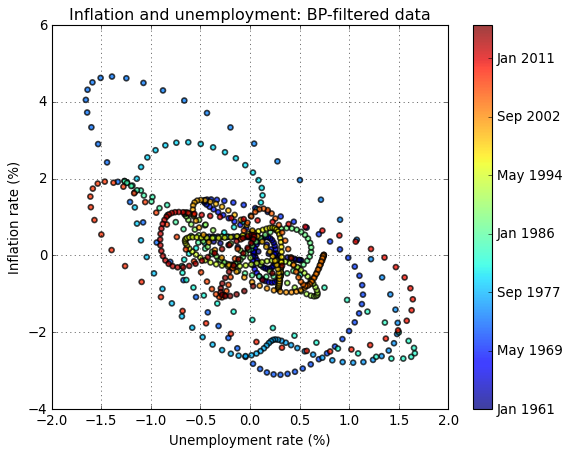

# Scatter plot of BP-filtered inflation and unemployment data (Sargent's Figure 1.5)

fig = plt.figure()

ax = fig.add_subplot(1,1,1)

t = np.arange(len(u_bpcycle.data))

plt.scatter(u_bpcycle.data,p_bpcycle.data,facecolors='none',alpha=0.75,s=20,c=t, linewidths=1.5)

ax.set_xlabel('Unemployment rate (%)')

ax.set_ylabel('Inflation rate (%)')

ax.set_title('Inflation and unemployment: BP-filtered data')

ax.grid(True)

cbar = plt.colorbar(ax = ax)

cbar.set_ticks([int(i) for i in cbar.get_ticks()[:-1]])

cbar.set_ticklabels([p_bpcycle.data.index[int(i)].strftime('%b %Y') for i in cbar.get_ticks()[:]])

[23]:

# HP filter

p_hpcycle,p_hptrend = p.hp_filter(lamb=129600)

u_hpcycle,u_hptrend = u.hp_filter(lamb=129600)

# Scatter plot of HP-filtered inflation and unemployment data (Sargent's Figure 1.5)

fig = plt.figure()

ax = fig.add_subplot(1,1,1)

t = np.arange(len(u_hpcycle.data))

plt.scatter(u_hpcycle.data,p_hpcycle.data,facecolors='none',alpha=0.75,s=20,c=t, linewidths=1.5)

ax.set_xlabel('Unemployment rate (%)')

ax.set_ylabel('Inflation rate (%)')

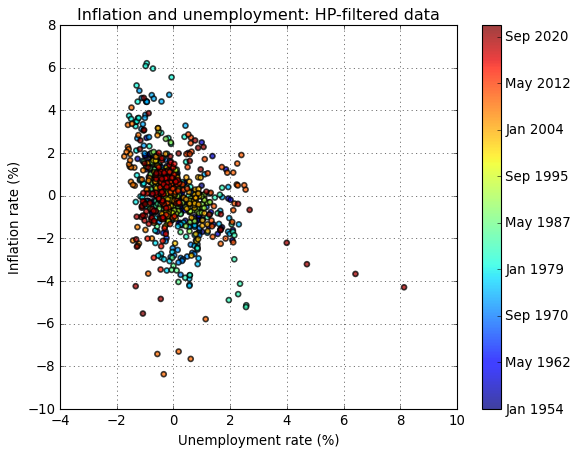

ax.set_title('Inflation and unemployment: HP-filtered data')

ax.grid(True)

cbar = plt.colorbar(ax = ax)

cbar.set_ticks([int(i) for i in cbar.get_ticks()[:-1]])

cbar.set_ticklabels([p_hpcycle.data.index[int(i)].strftime('%b %Y') for i in cbar.get_ticks()[:]])

The choice of filterning method appears to strongly influence the results. While both filtering methods produce a downward-sloping relationship between inflation and unemployment, the relationship is more pronounced in the BP-filtered data.

Vintage Data¶

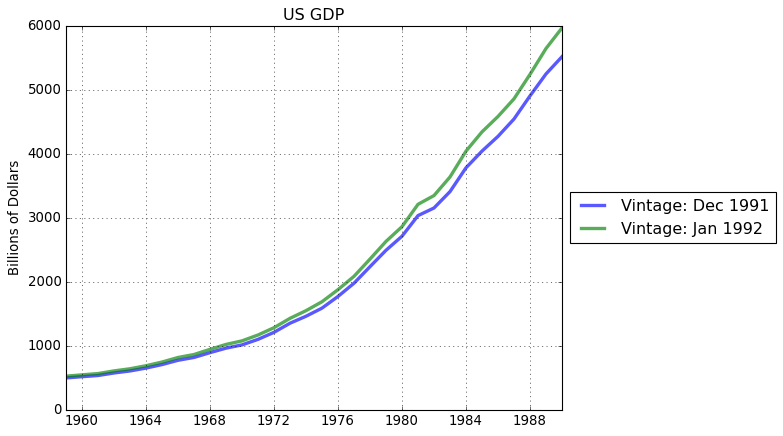

Data are updated and ALFRED, ArchivaL Federal Reserve Economic Data, stores historical data versions. Use get_vintage_dates() to find the avilable vintage dates for a FRED series. For example, let’s consider US GDP data.

[24]:

# Get all available vintages

gdp_vintage_dates = fp.get_vintage_dates('GDPA')

print('Number of vintages available:',len(gdp_vintage_dates))

print('Oldest vintage: ',gdp_vintage_dates[0])

print('Most recent vintage: ',gdp_vintage_dates[1])

Number of vintages available: 342

Oldest vintage: 1991-12-04

Most recent vintage: 1992-01-29

From the available vintage dates, use the observation_date keyword in series() to download a desired vintage. For example, download and plot the oldest available and most recent US GDP data.

[25]:

# Download oldest available GDP data

gdp_old = fp.series('GDPA',observation_date = gdp_vintage_dates[0])

# Download most recently available GDP data

gdp_cur = fp.series('GDPA',observation_date = gdp_vintage_dates[-1])

# Equalize date ranges

gdp_old, gdp_cur = fp.window_equalize([gdp_old, gdp_cur])

# Plot

fig = plt.figure()

ax = fig.add_subplot(1,1,1)

ax.plot(gdp_old.data,lw=3,alpha = 0.65,label=pd.to_datetime(gdp_vintage_dates)[0].strftime('Vintage: %b %Y'))

ax.plot(gdp_cur.data,lw=3,alpha = 0.65,label=pd.to_datetime(gdp_vintage_dates)[1].strftime('Vintage: %b %Y'))

ax.set_ylabel(gdp_cur.units)

ax.legend(loc='center left', bbox_to_anchor=(1, 0.5))

ax.set_title('US GDP')

ax.grid()

Exporting data sets¶

Exporting data inported with fredpy to csv files is easy with Pandas.

[26]:

# create a Pandas DataFrame

df = pd.DataFrame({'inflation':p.data,

'unemployment':u.data},)

print(df.head())

# Export to csv

df.to_csv('data.csv')

inflation unemployment

date

1954-01-01 0.338565 3.6

1954-02-01 -0.625714 3.8

1954-03-01 0.630199 4.1

1954-04-01 0.555030 4.7

1954-05-01 -0.557835 4.6

Custom API querries¶

The FRED API allows for more specific querries than what is available through the basic fredpy functionality. Read more about allowable querries to the API here: https://fred.stlouisfed.org/docs/api/fred/

In the cell below, I demonstrate how to manually retrieve unemployment data using the fredpy.fred_api_request() function.

[27]:

import datetime

# Specify the API path

path = 'fred/series/observations'

# Set observation_date string as today's date

observation_date = datetime.datetime.today().strftime('%Y-%m-%d')

# Specify desired parameter values for the API querry

parameters = {'series_id':'unrate',

'observation_date':observation_date,

'file_type':'json'

}

# API request

r = fp.fred_api_request(api_key=fp.api_key,path=path,parameters=parameters)

# Return results in JSON forma

results = r.json()

# Load data, deal with missing values, format dates in index, and set dtype

data = pd.DataFrame(results['observations'],columns =['date','value'])

data = data.replace('.', np.nan)

data['date'] = pd.to_datetime(data['date'])

data = data.set_index('date')['value'].astype(float)

# Plot the unemployment rate

data.plot()

plt.title('Unemployment Rate')

plt.grid()